April 2016 Dollar still under pressure |

|

|

|

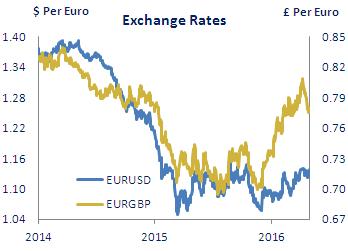

Overview The Fed left interest rates unchanged for a third consecutive meeting in April.It noted the continued strengthening of the labour market, even as economic growth eased in the opening quarter of the year, and dialled back its concerns about the potential impact of global developments on the US economy, while reiterating that interest rates are likely to increase albeit gradually. The ECB also left interest rates on hold in April and again said they are set to remain at present or lower levels for an extended period of time, with Mario Draghi also observing that monetary policy in the Euro area will continue to diverge from policy ‘in other jurisdictions better placed in the recovery cycle’ (a reference to the US). While this may be so, the euro has strengthened against the dollar over the past month as the market has pushed out the expected timing of the next increase in US interest rates into early next year. Meanwhile, having weakened in the opening quarter, sterling has regained a good deal of ground against both the euro and the dollar during April, though it is likely to remain volatile in the run up to the June referendum. |

|

Euro area GDP up 0.6% in Q1 |

|

Euro area growth picked up notably in Q1 2016, with GDP rising by 0.6% q-o-q according to the preliminary estimate (after increasing by 0.3% in Q4). On an annual basis the economy expanded by 1.6%, the same as in Q4. The IMF's latest forecasts envisage growth of 1.5% for 2016 as a whole, picking up slightly to 1.6% in 2017. Employment rose for a 9th consecutive quarter in Q4 and the unemployment rate has fallen to 10.2%, almost 2% points below its 2013 peak. Annual inflation remains subdued at -0.2%, while the core rate has been confined to a range of 0.8% to 1% since May 2015. The ECB left policy on hold in April and reiterated that interest rates are expected to remain at ‘present or lower levels for an extended period', while Mario Draghi noted that ‘our monetary policy course will continue to diverge from the monetary policy courses that prevail in other jurisdictions better placed in the recovery cycle’. Despite the substantial policy easing announced in March, the euro has since strengthened to around $1.14 against the dollar. |

|

|

|

UK growth eases in first quarter |

|

The UK economy grew by 0.4% q-o-q in Q1 2016, according to the preliminary GDP release (after expanding by 0.6% in Q4). Services sector activity eased a little albeit remaining quite strong, while output in manufacturing and construction fell. On an annual basis, GDP grew by 2.1%, the same as in Q4. The IMF expects full year growth of 1.9% (revised from 2.2% previously), picking up to 2.2% in 2017. The unemployment rate remained at 5.1% in the 3 months to February and average earnings (ex bonuses) rose by 2.2% y-o-y. Annual inflation ticked up to 0.5% in March and the core rate rose to 1.5%, its highest level since October 2014. The Bank of England’s MPC left interest rates unchanged at 0.5% in April and noted that uncertainty ahead of the EU referendum in June 'might lead to some softening in growth during the first half of 2016’. Having fallen sharply against the euro in Q1, sterling has recovered ground in April and is currently trading at around 78p. |

|

|

US growth slowed further in Q1 2016 according to preliminary estimates, with GDP rising by just 0.1% q-o-q (after increasing by 0.3% in Q4). The pace of consumer spending eased in the quarter and investment remained weak, while net exports were again a drag on GDP. The IMF expects annual growth of 2.4% this year, revised from 2.6% previously, and 2.5% in 2017. Notwithstanding slower growth, the labour market has continued to perform solidly. Employment rose by an average of 209,000 a month in Q1 and the unemployment rate fell to 4.9%, although the latter did tick up to 5% in March reflecting increasd participation in the labour force. Annual PCE inflation dipped to 0.8% in March and the core rate was running at 1.6%. Having first raised interest rates in December, the Fed stayed on hold for a third consecutive meeting in April but said that economic conditons are still likely to warrant 'gradual increases' in rates. |

|

|

|

|

This document has been prepared by the Economic Research Unit at The Governor and Company of the Bank of Ireland (“BOI”) for information purposes only and BOI is not soliciting any action based upon it. BOI believes the information contained herein to be accurate but does not warrant its accuracy nor accepts or assumes any responsibility or liability for such information other than any responsibility it may owe to any party under the European Communities (Markets in Financial Instruments) Regulations 2007 as may be amended from time to time, and under the Financial Conduct Authority rules (where the client is resident in the UK), for any loss or damage caused by any act or omission taken as a result of the information contained in this document. Any decision made by a party after reading this document shall be on the basis of its own research and not be influenced or based on any view or opinion expressed by BOI either in this document or otherwise. This document does not address all risks and cannot be relied on for any investment contract or decision. A party should obtain independent professional advice before making any investment decision. Expressions of opinion contained in this document reflect current opinion as at 29th April 2016 and is based on information available to BOI before that date. This document is the property of BOI and its contents may not be reproduced, either in whole or in part, without the express written consent of a suitably authorised member of BOI. |

The Governor and Company of the Bank of Ireland is regulated by the Central Bank of Ireland. In the UK, The Governor and Company of the Bank of Ireland is authorised by the Central Bank of Ireland and the Prudential Regulation Authority and subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our authorisation and regulation by the Prudential Regulation Authority and regulation by the Financial Conduct Authority are available from us on request. The Governor and Company of the Bank of Ireland is incorporated in Ireland with limited liability. Registered Office - 40 Mespil Road, Dublin 4, Ireland. |

|

|

|

|