May 2016 Fed raises prospect of June rate hike |

|

|

|

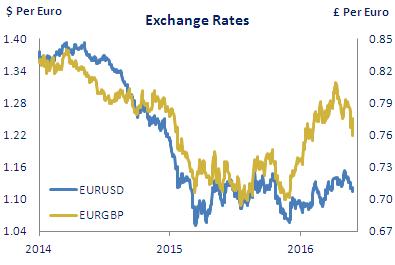

Overview The Fed left interest rates unchanged when it met in April and the accompanying policy statement gave no indication about what action it might take in June. However, the minutes of the meeting published subsequently revealed that a rate hike next month would be appropriate if economic growth picked up in the second quarter and labour market conditions continued to strengthen. Public statements from Fed officials since the release of the minutes have reinforced the message that June is a ‘live’ meeting for a possible rate increase. All of this has come as a surprise to the market, which had largely ruled out the likelihood of any increase in rates this year. It has now marked up the chances of a hike next month, which has led to a rise in US government bond yields and a strengthening of the dollar, albeit it puts the probability of a move at not much more than 30%. Arguably it should be higher, as recent data do suggest the economy is rebounding after a ‘soft patch’ in the first quarter and employment continued to increase at a healthy pace in April. Meanwhile, there has been a notable rebound in sterling over the past month as most polls show the Remain side in the lead ahead of the EU referendum on June 23. The UK currency has recovered to around 76p against the euro (from a low of 81p in early April), not much outside the 70-74p range that prevailed through most of 2015 before Brexit concerns began to take hold early in 2016. |

|

Euro gives up ground to dollar |

|

Having picked up in Q1 2016, hard and survey data indicate the pace of Euro area GDP growth may ease in Q2. Retail sales and industrial output ended Q1 on a weak note (both fell in March) and the composite PMI dipped to 52.9 in May according to the flash estimate, the weakest reading since January 2015. The EU Commission’s latest projections are for annual GDP growth of 1.6% this year (after 1.5% in 2015) and 1.8% in 2017. The labour market continues to improve with the unemployment rate falling further in March to a near 5-year low of 10.2%. However, slack in both the labour market and the economy generally still remains considerable judging by the subdued rate of both headline and core inflation (-0.2% and 0.7% respectively). The ECB left policy on hold in April as it assesses the impact of the measures announced in March. After strengthening to a 9-month high of over $1.16 against the dollar in early May, the euro has since fallen back to $1.12 as the possibility of a near-term Fed interest rate increase provides renewed support to the US currency. |

|

|

|

UK GDP growth seems to have moderated in Q2, at least judging by the available survey data. In particular, the composite PMI fell to 51.9 in April, with the services index declining to its lowest level since February 2013 and the manufacturing index recording its first sub 50 reading since March 2013. The Bank of England (BOE) noted in its May Inflation Report that uncertainty ahead of the EU referendum in June is weighing on activity. It now expects annual GDP growth to dip to 2.0% this year (from 2.3% in 2015) before picking up to 2.3% in 2017, albeit these forecasts assume the UK stays in the European Union. Meanwhile, the EU Commission is projecting an increase in GDP of 1.8% this year and 1.9% next. The unemployment rate remained at 5.1% in Q1, while annual headline and core inflation fell to 0.3% and 1.2% in April. The BOE's MPC kept interest rates steady at 0.5% in May and said that, ‘whatever the outcome of the referendum’, it will take ‘whatever action is needed’ to ensure inflation returns to the target’ of 2%. Sterling has strengthened by 6% to 76p against the euro as most polls show a shift in favour of a vote to remain in the EU. |

|

|

Activity in the US economy looks to have picked up in Q2 after GDP growth slowed to 0.2% q-o-q in Q1. Retail sales rebounded strongly in April, rising by 1.3% m-o-m, while the ISM non-manufacturing (i.e. mainly services) index rose for a second consecutive month and is now running ahead of its average level in Q1. Employment increased by 160,000 in April and the unemployment rate remained at 5%, while earnings growth accelerated to 2.5% year-on-year. Annual PCE inflation has dipped below 1% but the core rate remains steady at 1.6-1.7%. The Fed kept interest rates unchanged in April but the minutes of the meeting (released in mid-May) noted that a June hike ‘likely would be appropriate’ if incoming data ‘were consistent with economic growth picking up in the second quarter and labour market conditions continuing to strengthen’. The market has raised the probability of a rate increase next month albeit to not much more than 30%. This has led to an increase in government bond yields, with 2-year yields almost 20bps off their recent lows, and to a strengthening of the dollar. |

|

|

|

|

This document has been prepared by the Economic Research Unit at The Governor and Company of the Bank of Ireland (“BOI”) for information purposes only and BOI is not soliciting any action based upon it. BOI believes the information contained herein to be accurate but does not warrant its accuracy nor accepts or assumes any responsibility or liability for such information other than any responsibility it may owe to any party under the European Communities (Markets in Financial Instruments) Regulations 2007 as may be amended from time to time, and under the Financial Conduct Authority rules (where the client is resident in the UK), for any loss or damage caused by any act or omission taken as a result of the information contained in this document. Any decision made by a party after reading this document shall be on the basis of its own research and not be influenced or based on any view or opinion expressed by BOI either in this document or otherwise. This document does not address all risks and cannot be relied on for any investment contract or decision. A party should obtain independent professional advice before making any investment decision. Expressions of opinion contained in this document reflect current opinion as at 27th May 2016 and is based on information available to BOI before that date. This document is the property of BOI and its contents may not be reproduced, either in whole or in part, without the express written consent of a suitably authorised member of BOI. |

The Governor and Company of the Bank of Ireland is regulated by the Central Bank of Ireland. In the UK, The Governor and Company of the Bank of Ireland is authorised by the Central Bank of Ireland and the Prudential Regulation Authority and subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our authorisation and regulation by the Prudential Regulation Authority and regulation by the Financial Conduct Authority are available from us on request. The Governor and Company of the Bank of Ireland is incorporated in Ireland with limited liability. Registered Office - 40 Mespil Road, Dublin 4, Ireland. |

|

|

|

|