August 2016 Case for US rate hike 'has strengthened' |

|

|

|

Overview The Bank of England (BoE) has eased monetary policy in response to a weaker outlook for the UK economy following the Brexit vote in late June. It has cut interest rates by 25bps to 0.25%, reactivated its QE programme - it will purchase £70bn of assets over the coming months - and introduced a new funding scheme for banks. Moreover, the BoE says it is prepared to take further action if required, including cutting interest rates to ‘a little above zero’. Meanwhile, the ECB says that, in light of the 'still high level of slack' and continuing ‘weak wage and price pressures’ in the Euro Area economy, it will be necessary to consider ‘the time horizon over which a very accommodative monetary policy stance would remain warranted’. This suggests it may be prepared to extend its QE programme beyond the planned end date of March 2017. In contrast, the Fed Chair, Janet Yellen, has noted that the case for an increase in US interest rates ‘has strengthened’ in recent months given the continuing improvement in the labour market. A rate hike as soon as the September 20-21 meeting is now certainly possible, something that would provide support to the dollar. |

|

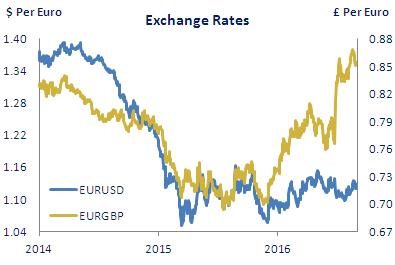

Exchange Rates (Economic Research Unit) |

|

|

5-Year Swaps (Indicative Market Forward Rates) |

|

|

|

|

Euro area inflation very subdued |

|

Euro area GDP rose by 0.3% q-o-q in Q2 and the latest survey data point to a similar pace of growth in Q3. In particular, the composite PMI averaged 53.3 in July-August, broadly in line with its Q2 reading. The unemployment rate is nudging lower, though at 10.1% it is still some 3% points above its pre-crisis low in early 2008. Headline inflation remains very subdued at just 0.2%, while the core rate has been stable but still relatively low at just under 1%. The ECB left policy unchanged in July, saying it was too early to assess the impact of the Brexit vote in the UK on the Euro Area economy, and hence too soon to consider any response, but would continue to ‘closely monitor developments’. More generally, it said that ‘in the current environment of...a still high level of economic slack and weak wage and price pressures', a discussion 'was called for regarding…the time horizon over which a very accommodative monetary policy stance would remain warranted'. This suggests the ECB may be prepared to extend QE beyond the planned end date of March 2017 and/or commit to keeping interest rates at the present very low level for a considerable period of time yet. |

|

|

|

Mixed economic data in the UK |

|

GDP growth in the UK strengthened to 0.6% q-o-q in Q2. Consumer spending was the main driver of activity, though investment rebounded having fallen in the two previous quarters. The post EU referendum data paint a mixed picture. On the one hand, the composite PMI fell in July to 47.5, consistent with a contraction in activity. On the other, retail sales rose strongly in July suggesting consumer spending is still contributing significantly to growth. The BoE expects the economy to slow over H2 2016 and into 2017 and has revised down its forecasts accordingly. It also expects inflation to rise noticeably, largely on account of sterling’s fall, but has responded to the weaker growth outlook by cutting interest rates (by 25bps to 0.25%) and reactivating QE (it will purchase £60bn of government bonds and £10bn in corporate bonds over the coming months). It has also said that it may cut rates again (to just above 0%) before end-year. Government bond yields have fallen to record lows following the BOE’s action and corporate spreads have tightened, while sterling weakened to fresh lows of over 87p against the euro before recovering to 85p. |

|

|

US jobs growth strengthens |

|

Growth in the US economy picked up in Q2 2016 with GDP rising by 0.3% q-o-q. Consumer spending strengthened, rising at its fastest pace in over a year, but investment fell and a run-down of stocks weighed on growth. The available indicator data point to a further pick-up in activity in Q3. Industrial output rose for a second month running in July, and the ISM manufacturing and non-manufacturing indices were both running ahead of Q2. Jobs growth has strengthened, with employment rising by 255,000 in July, and the unemployment rate continues to trend lower. Annual PCE inflation eased in July while the core rate remained steady at 1.6%. The Fed left policy on hold at its meeting in July, but the minutes showed that ‘some members anticipated that economic conditions would soon warrant’ an increase in interest rates. In subsequent remarks, the Fed Chair, Janet Yellen, said the case for a rate hike ‘has strengthened’ in light of the continuing improvement in the labour market, which means such a move at the September 20-21 meeting is now certainly possible. |

|

|

|

|

Forward swap rates are sourced from Bloomberg and are calculated from live prevailing market interest rates and reflect market pricing as at 31/08/2016. |

Disclaimer This document has been prepared by the Economic Research Unit at The Governor and Company of the Bank of Ireland (“BOI”) for information purposes only and BOI is not soliciting any action based upon it. BOI believes the information contained herein to be accurate but does not warrant its accuracy nor accepts or assumes any responsibility or liability for such information other than any responsibility it may owe to any party under the European Communities (Markets in Financial Instruments) Regulations 2007 as may be amended from time to time, and under the Financial Conduct Authority rules (where the client is resident in the UK), for any loss or damage caused by any act or omission taken as a result of the information contained in this document. Any decision made by a party after reading this document shall be on the basis of its own research and not be influenced or based on any view or opinion expressed by BOI either in this document or otherwise. This document does not address all risks and cannot be relied on for any investment contract or decision. A party should obtain independent professional advice before making any investment decision. Expressions of opinion contained in this document reflect current opinion as at 31st August 2016 and is based on information available to BOI before that date. This document is the property of BOI and its contents may not be reproduced, either in whole or in part, without the express written consent of a suitably authorised member of BOI. |

The Governor and Company of the Bank of Ireland is regulated by the Central Bank of Ireland. In the UK, The Governor and Company of the Bank of Ireland is authorised by the Central Bank of Ireland and the Prudential Regulation Authority and subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our authorisation and regulation by the Prudential Regulation Authority and regulation by the Financial Conduct Authority are available from us on request. The Governor and Company of the Bank of Ireland is incorporated in Ireland with limited liability. Registered Office - 40 Mespil Road, Dublin 4, Ireland. |

|

|

|

|