November 2016 Dollar jumps on Trump |

|

|

|

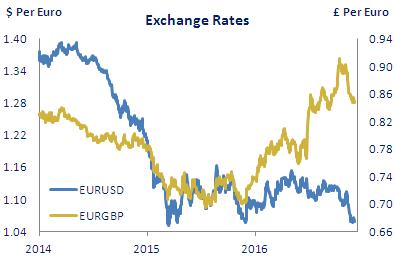

Overview The election result in the US has triggered a rise in bond yields and a strengthening of the dollar, as the market sees the new administration implementing a ‘fiscal stimulus’ package to boost growth (and that will probably also lead to higher inflation). In addition, a pick up in economic activity in Q3 and continuing solid job gains have convinced the market that the Fed will hike interest rates in December and raise them further during 2017, which has also contributed to higher yields and the stronger dollar. The latter, though, still remains within the $1.05 to $1.15 range against the euro that has prevailed since March 2015, and any further sustained strengthening may have to await clarity on Trump's fiscal plans (and the Fed's possible response). Meanwhile, sterling has recovered some ground against the single currency over the past month, strengthening to around 85p having fallen to over 91p following the Brexit vote and after the Bank of England (BOE) cut interest rates and reactivated QE. The recent resilience of the UK economy has led the market to ‘price out’ any further cut in interest rates and it now considers a hike as more probable albeit not until 2018. This has supported sterling, as has the High Court ruling that the UK parliament must have a say in triggering Article 50. However, most forecasts see the economy slowing next year and so a further cut in interest rates cannot be ruled out, particularly if growth weakens by more than the BOE currently expects. Sterling would probably lose ground in those circumstances and in any case is likely to come under pressure again in the run up to the triggering of Article 50, which the government insists will be by the end of March next year. In the near-term, though, the outcome of the impending constitutional referendum in Italy has the potential to cause increased volatility in the currency market. |

|

Exchange Rates (Economic Research Unit) |

|

|

5- Year Swaps (Indicative market forward rates) |

|

|

|

|

Euro area GDP up 0.3% in Q3 |

|

The Euro area economy expanded by 0.3% q-o-q in Q3 according to the latest GDP estimate, and the pace of activity may have ticked up in the final quarter of the year judging by the ‘flash' composite PMI. It rose for a third consecutive month in November to a 2016 high of 54.1, with the manufacturing and services PMIs both increasing. The OECD expects annual GDP growth to average 1.7% this year and 1.6% in 2017, the latter revised up from 1.4% in its September update, though it expects ‘investment weakness to persist reflecting…banking sector fragilities and uncertainties about European integration’. The unemployment rate has fallen by more than half a percentage point in 2016 to date and currently stands at 9.8%, down from a peak of just over 12.0% in mid-2013. Headline inflation nudged higher again in November, to 0.6%, but the core rate remained unchanged for a fourth month running at 0.8%. The ECB has reiterated that it is necessary to maintain an ‘expansionary monetary stance’ until inflation is on a ‘sustained path’ back towards the target of just below 2%, suggesting it may announce an extension of its QE programme, perhaps at its next meeting on December 8. |

|

|

|

BOE leaves rates unchanged |

|

The UK economy remained resilient in Q3, with the pace of GDP growth easing only slightly to 0.5% q-o-q (from 0.7% in Q2). Consumer spending was an important driver of growth again, and business investment rose for a second consecutive quarter (though it continued to run below year-earlier levels), while net exports made a positive contribution to GDP (helped by sterling weakness). In its Autumn Statement, the government ‘opted neither for a large near-term fiscal stimulus nor for more austerity over the medium term’ according to the Office of Budget Responsibility (OBR), which following the Brexit vote has revised down its forecasts for GDP growth in 2017 and 2018 to 1.4% and 1.7% respectively (from 2.2% and 2.1% in March). The OBR’s projections are more optimistic than those of the OECD, which is forecasting an increase in GDP of 1.2% in 2017 and just 1.0% in 2018, though they are broadly in line with those of the Bank of England (BOE). Headline inflation dipped to 0.9% in October and the core rate fell back to 1.2%. The BOE expects inflation to pick up to 2.7% over the course of next year, even as growth is forecast to slow, due largely to sterling’s decline. It left interest rates unchanged in November and stated that monetary policy ‘will respond, in either direction, to changes in the economic outlook as they unfold’. |

|

|

Economic activity in the US picked up in Q3, after a lacklustre first half of 2016, with GDP increasing by 0.8% q-o-q, the fastest pace of growth in 2 years. Consumer spending rose solidly in the quarter and both net exports and stock-building made positive contributions to growth. The OECD expects GDP to increase by 2.3% in 2017 (revised up from 2.1%) and 3.0% in 2018, with an ‘assumed fiscal stimulus’ following Donald Trump’s election as president projected to boost growth. The prospect of a fiscal stimulus has triggered a sharp rise in US bond yields - of almost 60bps in the case of 10-year yields - and a strengthening of the dollar against other major currencies, notably the yen and the euro. Employment continues to rise steadily (with payroll gains averaging 176,000 a month in August-October) and the unemployment remains below 5%, while headline PCE inflation has risen to a 2 year high of 1.4%. The Fed left interest rates unchanged at its November meeting but reiterated that the case for an increase ‘has continued to strengthen’, while Janet Yellen subsequently stated that such an increase ‘could well become appropriate relatively soon’. Reflecting this, the market has now fully ‘priced in’ a 25bps hike in rates at the Fed’s December 13/14 meeting. |

|

|

|

|

Forward rates are sourced from Bloomberg and are calculated from live prevailing market interest rates and reflect market pricing as at 30/11/2016. |

Disclaimer This document has been prepared by the Economic Research Unit at The Governor and Company of the Bank of Ireland (“BOI”) for information purposes only and BOI is not soliciting any action based upon it. BOI believes the information contained herein to be accurate but does not warrant its accuracy nor accepts or assumes any responsibility or liability for such information other than any responsibility it may owe to any party under the European Communities (Markets in Financial Instruments) Regulations 2007 as may be amended from time to time, and under the Financial Conduct Authority rules (where the client is resident in the UK), for any loss or damage caused by any act or omission taken as a result of the information contained in this document. Any decision made by a party after reading this document shall be on the basis of its own research and not be influenced or based on any view or opinion expressed by BOI either in this document or otherwise. This document does not address all risks and cannot be relied on for any investment contract or decision. A party should obtain independent professional advice before making any investment decision. Expressions of opinion contained in this document reflect current opinion as at 2nd December 2016and is based on information available to BOI before that date. This document is the property of BOI and its contents may not be reproduced, either in whole or in part, without the express written consent of a suitably authorised member of BOI. |

The Governor and Company of the Bank of Ireland is regulated by the Central Bank of Ireland. In the UK, The Governor and Company of the Bank of Ireland is authorised by the Central Bank of Ireland and the Prudential Regulation Authority and subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our authorisation and regulation by the Prudential Regulation Authority and regulation by the Financial Conduct Authority are available from us on request. The Governor and Company of the Bank of Ireland is incorporated in Ireland with limited liability. Registered Office - 40 Mespil Road, Dublin 4, Ireland. |

|

|

|

|