December 2016 An event-full 2017 |

|

|

|

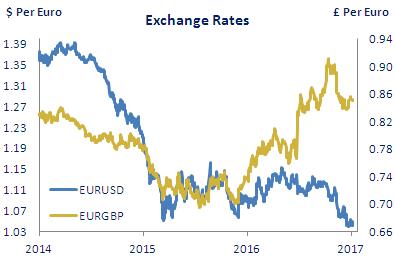

Overview 2017 promises to be just as eventful as 2016, with perhaps another few surprises too! Later this month, Donald Trump assumes the presidency of the US and the markets (and the world) will be anxious to learn what follows; the UK government plans to trigger Article 50 by the end of March and so begin the process of negotiating the UK’s withdrawal from the EU; and in Europe, elections take place in the Netherlands, France and Germany (and possibly Italy). Plenty there, then, to suggest markets will be volatile again this year. The major central banks have also set out their monetary policy stalls for 2017. The ECB has announced an extension of its QE programme by 9 months to the end of this year, given the absence to date of any convincing signs of a pick-up in underlying inflation in the Euro area. It has also made clear that it is keen to maintain its ‘presence’ in the market given the potential for increased political and economic uncertainty. In the US, the Fed raised interest rates by 25bps in December and ‘guided’ a further three quarter-point hikes this year, up from two previously, while also noting that any fiscal ‘stimulus’ might mean that rates would have to increase by more than currently anticipated. All of this resulted in EUR/$ breaking out of its long-standing trading range (of $1.05 to $1.15) during December with the dollar strengthening to around $1.0350. It has eased back a bit since, but a renewed move higher is likely. Meanwhile, sterling has given up some ground against the euro recently to trade back at 85p.The Bank of England has warned of ‘further volatility in the sterling exchange rate' ahead, and we still see it weakening against the euro over the coming months. |

|

UK PMI data positive in Q4 |

|

|

Exchange Rates (Economic Reaearch Unit) |

|

|

5-Year Swaps (Indicative Market Forward Rates) |

|

|

|

|

Euro area inflation above 1% |

|

The Euro area economy expanded by 0.3% q-o-q in Q3 2016 according to the third and final estimate of GDP, with an increase in domestic demand more than offsetting a negative contribution from net exports. The PMI data suggest the pace of growth might have picked up slightly in the final quarter of the year - the composite index rose to 53.9 from 52.9 in Q3 and stood at 54.4 in December. The labour market continues to improve gradually, with employment rising again in Q3 and the unemployment rate falling further in October to 9.8%. Headline inflation is picking up and stood at 1.1% in December according to the flash estimate, the first reading above 1% in more than 3 years. Core (or underlying) inflation remains ‘sticky’, however, at just under 1%. The ECB announced a 9 month extension of its QE programme at its December meeting, noting that there are no convincing signs yet of a pick up in core inflation. It will continue to buy assets at a pace of €80bn per month up until March, and then €60 a month from April through to December. It also said it is prepared to increase the programme - in terms of its size and/or duration - if that proves warranted. |

|

|

|

UK PMI data positive in Q4 |

|

Economic growth in the UK was slightly stronger in Q3 2016 than initially estimated, with GDP increasing by 0.6% q-o-q, and looks to have remained quite resilient again in Q4. The composite PMI averaged 55.3 in the three months to December, up from 51.6 in the third quarter, and ended 2016 at a seventeen month high of 56.2, while retail sales rose by almost 6% on an annual basis in November. There have been more mixed developments in the labour market, however, with the numbers in employment dipping slightly in the three months to October albeit the unemployment rate remained at 4.8%. Annual inflation rebounded in November, rising to a more than 2 year high of 1.2%, while the core rate picked up to 1.4%. The Bank of England kept policy on hold at its December meeting. While noting that ‘growth appeared to have been remarkably stable during 2016’, it said it still expects ‘some slowing in activity in 2017’. It also noted that sterling’s recent recovery ‘all else equal would result in a slightly lower path for inflation than envisaged in the November Inflation Report, though it is still likely to overshoot the target later in 2017 and through 2018’. |

|

|

Fed raises interest rates |

|

GDP growth in the US in Q3 2016 was revised up slightly to 0.8% q-o-q and 1.7% y-o-y, with consumer spending increasing more strongly than previously estimated. Activity seems to have expanded at a solid pace again in Q4, judging by the available indicator data. The ISM Index of manufacturing rose to a 2 year high of 54.7 in December and averaged 53.3 in Q4, up from 51.2 in Q3, while the equivalent non-manufacturing index in October-November was also running ahead of its level in the third quarter. Consumer spending rose by 2.8% y-o-y in November, in line with the rate of growth recorded in Q3. Spending is being supported by the on-going strengthening of the labour market - employment rose by 178,000 in November and the unemployment rate fell to 4.6%, its lowest level since July 2007. Annual PCE inflation is edging up and stood at 1.4% in November, more than 1% point higher than a year earlier. The Fed raised interest rates by 25bps (to a range of 0.50% to 0.75%) at its December meeting and ‘guided’ a further three quarter point hikes in 2017, up from two previously. |

|

|

|

|

Forward rates are sourced from Bloomberg and are calculated from live prevailing market interest rates and reflect market pricing as at 5/01/2017. |

Disclaimer This document has been prepared by the Economic Research Unit at The Governor and Company of the Bank of Ireland (“BOI”) for information purposes only and BOI is not soliciting any action based upon it. BOI believes the information contained herein to be accurate but does not warrant its accuracy nor accepts or assumes any responsibility or liability for such information other than any responsibility it may owe to any party under the European Communities (Markets in Financial Instruments) Regulations 2007 as may be amended from time to time, and under the Financial Conduct Authority rules (where the client is resident in the UK), for any loss or damage caused by any act or omission taken as a result of the information contained in this document. Any decision made by a party after reading this document shall be on the basis of its own research and not be influenced or based on any view or opinion expressed by BOI either in this document or otherwise. This document does not address all risks and cannot be relied on for any investment contract or decision. A party should obtain independent professional advice before making any investment decision. Expressions of opinion contained in this document reflect current opinion as at 5th January 2017 and is based on information available to BOI before that date. This document is the property of BOI and its contents may not be reproduced, either in whole or in part, without the express written consent of a suitably authorised member of BOI. |

The Governor and Company of the Bank of Ireland is regulated by the Central Bank of Ireland. In the UK, The Governor and Company of the Bank of Ireland is authorised by the Central Bank of Ireland and the Prudential Regulation Authority and subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our authorisation and regulation by the Prudential Regulation Authority and regulation by the Financial Conduct Authority are available from us on request. The Governor and Company of the Bank of Ireland is incorporated in Ireland with limited liability. Registered Office - 40 Mespil Road, Dublin 4, Ireland. |

|

|

|

|