February 2017 A more active Fed |

|

|

|

Overview While markets still await details of the new US administration’s economic policies, the Fed is re-entering the scene sooner than might have been expected. After waitng for a year before raising interest rates for a second time last December, it seems to be gearing up to hike again later this month judging by recent public commentary. One influential member (Dudley) noted that the case for another increase has become ‘a lot more compelling’ based on the economic data that have been published over the past couple of months. In particular, employment growth has remained solid - a further 227,000 jobs were added in January - and inflation has picked up to 1.9%, just shy of the Fed’s 2% target. Having prompted the markets to price in a high probability (more than 80%) of a 25bps hike later this month, the Fed is likely to follow through and deliver. Meanwhile, growth in the Euro area appears to have picked up at the start of 2017, unemployment is falling steadily and headline inflation has accelerated to 2% albeit the core rate remains below 1%. Depending on how political developments unfold over the coming months, debate could intensify towards the end of this year about the degree of monetary policy support the ECB needs to continue providing to the economy. In the meantime, a more active Fed means rising US interest rates are likely to underpin the dollar in the period ahead. |

|

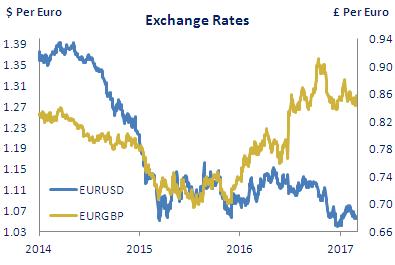

Exchange Rates (Economic Research Unit) |

|

|

5- Year Swap Rates (Indicative Market Forward Rates) |

|

|

|

|

GDP growth in the Euro area in Q4 2016 was revised down a touch to 0.4% q-o-q (from 0.5%), though the high frequency data point to an acceleration in activity in Q1 2017. In particular, the composite PMI rose to 56.0 in February, its highest level since April 2011. The EU Commission is projecting annual GDP growth of 1.6% this year, rising to 1.8% in 2018. Headline inflation has picked up noticeably in recent months to 2.0%, though this is primarily due to rising food and energy price inflation. Excluding both of these, the underlying (or core) rate of inflation remains low and sticky at just under 1%. At the ECB’s January meeting, President Draghi again acknowledged ‘that there are no signs yet of a convincing upward trend in underlying inflation’ and said ‘a substantial degree of monetary accommodation is needed for…inflation pressures to build up and support headline inflation'. |

|

|

|

Signs UK growth may be easing |

|

GDP in the UK rose at a slightly stronger pace in Q4 last year (0.7% q-o-q) than first estimated, though annual growth for 2016 as a whole was revised down to 1.8% (from 2.0%). Meanwhile, high frequency data suggest the pace of activity may be easing at the start of 2017. Most notably perhaps, retail sales fell in January and were running well below their level in Q4, while the composite PMI eased back in both January and February. In its latest forecasts, the EU Commission is projecting annual GDP growth to slow to 1.5% in 2017 and to 1.2% in 2018. Job gains moderated in Q4 2016, with employment increasing by 37,000 from Q3, though the unemployment rate remained at 4.8%, while headline inflation picked up further in January to 1.8%. The market has scaled back the likelihood of the BoE raising interest rates over the next year and now puts the chances of a hike at around 20% (from 80% a month ago). |

|

|

Fed gearing up to hike again |

|

Though the US economy grew in 2016 at its slowest pace since 2011, activity picked up over the second half of the year and the positive momentum appears to have carried into 2017. The ISM manufacturing index, for example, rose for a 6th consecutive month in February, led by a very strong increase in new orders, to stand at its highest level since August 2014. Consumer spending is underpinning growth in the economy and continues to be supported by solid employment gains. More than 2 million jobs were added in 2016 with a further increase of 227.000 in January, while the unemployment rate is below 5%. Inflation has picked up recently and is currently running at 1.9%, the highest reading since October 2012 and close to the Fed’s 2% target. The Fed left interest rates on hold in January but recent public commentary suggests a hike may be in the offing at this month’s meeting (March 14-15). |

|

|

|

|

Forward rates are sourced from Bloomberg and are calculated from live prevailing market interest rates and reflect market prcing as at 03/03/2017 |

Disclaimer This document has been prepared by the Economic Research Unit at The Governor and Company of the Bank of Ireland (“BOI”) for information purposes only and BOI is not soliciting any action based upon it. BOI believes the information contained herein to be accurate but does not warrant its accuracy nor accepts or assumes any responsibility or liability for such information other than any responsibility it may owe to any party under the European Communities (Markets in Financial Instruments) Regulations 2007 as may be amended from time to time, and under the Financial Conduct Authority rules (where the client is resident in the UK), for any loss or damage caused by any act or omission taken as a result of the information contained in this document. Any decision made by a party after reading this document shall be on the basis of its own research and not be influenced or based on any view or opinion expressed by BOI either in this document or otherwise. This document does not address all risks and cannot be relied on for any investment contract or decision. A party should obtain independent professional advice before making any investment decision. Expressions of opinion contained in this document reflect current opinion as at 3rd March 2017 and is based on information available to BOI before that date. This document is the property of BOI and its contents may not be reproduced, either in whole or in part, without the express written consent of a suitably authorised member of BOI. |

The Governor and Company of the Bank of Ireland is regulated by the Central Bank of Ireland. In the UK, The Governor and Company of the Bank of Ireland is authorised by the Central Bank of Ireland and the Prudential Regulation Authority and subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our authorisation and regulation by the Prudential Regulation Authority and regulation by the Financial Conduct Authority are available from us on request. The Governor and Company of the Bank of Ireland is incorporated in Ireland with limited liability. Registered Office - 40 Mespil Road, Dublin 4, Ireland. |

|

|

|

|