April 2017 ECB not for turning yet |

|

|

|

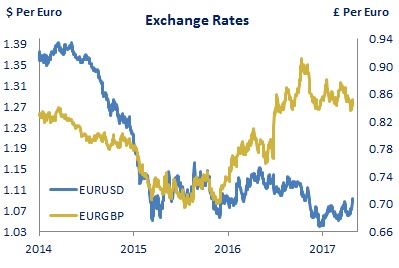

Overview The UK PM’s surprise decision to call a general election for June 8 prompted a jump in sterling to a 9-month high of 83.5p against the euro, although it gave up some of these gains following the result of the 1st round of voting in the French presidential election. This showed the independent centrist candidate, Emmanuel Macron, ahead on 24% of the vote and, according to the polls, on track to defeat Marine Le Pen in the 2nd round run-off on May 7. Markets were reassured by the outcome, judging by their initial reaction, with European equities rallying, French bond yield spreads over Germany narrowing, and the euro strengthening. Despite an uncertain political backdrop, the Euro area economy appears to have gained momentum in the opening months of 2017, with the (flash) composite PMI rising to a 6-year high in April. The ECB has acknowledged the improving outlook, but has also reiterated its view that substantial monetary support (via QE and continued low interest rates) remains necessary to underpin the recovery and help inflation get back to target on a sustainable basis. In the US, growth slowed in the opening quarter of the year, but that did not prevent continuing solid job gains pushing the unemployment rate down to a pre-global crisis low of 4.5% in March. This keeps the Fed on track to raise interest rates further over the coming months, which should be accompanied by a renewed strengthening of the dollar against the euro albeit remaining within its recent trading range. Meanwhile, with Brexit negotiations getting underway soon and evidence that the UK economy is starting to slow, sterling may lose some ground against the euro in the period ahead (though remaining within its recent range). |

|

Exchange Rates (Economic Research Unit) |

|

|

5-Year Swaps (Indicative Market Rates) |

|

|

|

|

Euro Area PMI at a 6-year high |

|

The pace of economic growth in the Euro area appears to have strengthened in the opening months of 2017, judging by the high frequency data. In particular, the composite PMI has risen steadily since the start of the year, and reached a 6-year high of 56.7 in April according to the flash reading, with activity in both manufacturing and services picking up over this period. The IMF has revised up its forecast for GDP growth this year a touch to 1.7%, and expects the economy to expand by 1.6% in 2018. The labour market also continues to improve and the unemployment rate is down to a near 8-year low of 9.5% (February). Having fallen in March, following a sharp rise over the previous three months, the annual inflation rate picked up to 1.9% in April with the core rate rebounding to 1.2%. The ECB acknowledged the improving outlook for the economy at its April meeting, but again said that a very substantial degree of monetary policy support is needed to ensure that inflation returns to its target (of just under 2%) on a sustainable basis. |

|

|

|

UK growth slows in first quarter |

|

According to preliminary estimates, GDP growth in the UK eased to 0.3% q-o-q in Q1 2017 from 0.7% in Q4, mainly due to slowing growth in the services sector. This in turn partly reflects weaker household spending, with separate data showing retail sales fell by 1.4% (q-o-q) in Q1. Incomes are being squeezed by higher inflation, which at 2.3% is running slightly ahead of the rate of increase in earnings (ex bonuses), while employment gains have slowed, both of which are weighing on spending. The IMF expects GDP to increase by 2.0% in 2017 - though the pace of growth is forecast to moderate over the course of the year - and by 1.5% in 2018. The Bank of England left policy on hold in March and again said interest rates can respond in either direction to changes in the economic outlook as they evolve. Meanwhile, PM May's announcement of a June election prompted a 1.5p jump in sterling (to 83.5p) against the euro, though it subsequently gave up some of these gains. |

|

|

GDP in the US up 0.2% in Q1 |

|

GDP growth in the US slowed to 0.2% q-o-q in Q1 2017 (from 0.5% in Q4), with an easing in the pace of consumer spending only partially offset by stronger investment and exports. The economy expanded by 1.9% on an annual basis in Q1, and the IMF expects full-year growth to average 2.3% in 2017 before strengthening to 2.5% in 2018. Job gains remained solid in the first quarter and the unemployment rate fell to a pre-global crisis low of 4.5% in March. Annual PCE inflation picked up in February to 2.1%, slightly above the Fed’s 2% target. As it had well flagged in advance, the Fed raised interest rates by 25bps in March and ‘guided’ a further two quarter-point increases this year. The Trump administration has provided a broad outline of its tax plan, which includes cuts in the standard corporate tax rate and top personal income tax rate as well as a profit repatriation tax, though it does not contain a border-adjusted tax (BAT). |

|

|

|

|

Forward rates are sourced from Bloomberg and are calculated from live prevailing market interest rates and reflect market prcing as at 28/04/2017 |

Disclaimer This document has been prepared by the Economic Research Unit at The Governor and Company of the Bank of Ireland (“BOI”) for information purposes only and BOI is not soliciting any action based upon it. BOI believes the information contained herein to be accurate but does not warrant its accuracy nor accepts or assumes any responsibility or liability for such information other than any responsibility it may owe to any party under the European Communities (Markets in Financial Instruments) Regulations 2007 as may be amended from time to time, and under the Financial Conduct Authority rules (where the client is resident in the UK), for any loss or damage caused by any act or omission taken as a result of the information contained in this document. Any decision made by a party after reading this document shall be on the basis of its own research and not be influenced or based on any view or opinion expressed by BOI either in this document or otherwise. This document does not address all risks and cannot be relied on for any investment contract or decision. A party should obtain independent professional advice before making any investment decision. Expressions of opinion contained in this document reflect current opinion as at 28th April 2017 and is based on information available to BOI before that date. This document is the property of BOI and its contents may not be reproduced, either in whole or in part, without the express written consent of a suitably authorised member of BOI. |

The Governor and Company of the Bank of Ireland is regulated by the Central Bank of Ireland. In the UK, The Governor and Company of the Bank of Ireland is authorised by the Central Bank of Ireland and the Prudential Regulation Authority and subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our authorisation and regulation by the Prudential Regulation Authority and regulation by the Financial Conduct Authority are available from us on request. The Governor and Company of the Bank of Ireland is incorporated in Ireland with limited liability. Registered Office - 40 Mespil Road, Dublin 4, Ireland. |

|

|

|

|