June 2017 Euro extends gains |

|

|

|

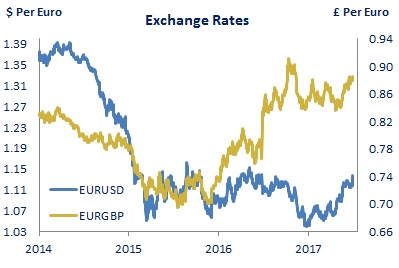

Overview The Fed raised interest rates by 25bps at its June meeting, and signalled one more increase is likely this year followed by 3 further hikes in 2018. It also outlined a plan to reduce the size of its balance sheet, which it said could commence relatively soon. Meanwhile, the Bank of England’s MPC kept interest rates unchanged at its latest policy meeting but 3 of the 8 members voted for an immediate 25bps increase, a greater degree of dissent than the market had expected. Nevertheless, despite these developments, both sterling and the dollar have lost ground against the euro, falling to 88p and $1.14 respectively. Supporting the single currency at present is the markets’ focus on what may be an inflection point for the ECB’s monetary policy. The ECB is currently providing substantial support to the Euro area economy via asset purchases (QE) and zero/negative interest rates. Its asset purchases of €60bn per month are scheduled to run until the end of this year or beyond if necessary and, according to the ECB, interest rates are expected to remain at their present level for an extended period. However, Mario Draghi has said that, as the economic recovery proceeds, it will be necessary to gradually adjust ‘our policy parameters’. This adjustment may involve, in the first instance, the ECB reducing (‘tapering') the pace of asset purchases from the start of 2018, with an announcement along these lines possible over the next few months, perhaps at the next but one meeting in September. Such a prospect is likely to underpin the euro in the meantime, though further policy tightening in the US and the possibility of a rate hike in the UK may cap the downside for the dollar and sterling. |

|

Exchange Rates (Economic Research Unit) |

|

|

5-Year Swaps (Indicative Market Rates) |

|

|

|

|

Euro area recovery continuing |

|

Q1 growth in the Euro area was slightly stronger than initially estimated, with GDP increasing by 0.6% q-o-q and by 1.9% on an annual basis. Investment posted a sizeable increase and consumer spending rose for a 12th consecutive quarter, though net exports made little or no contribution to the increase in GDP. The high frequency data indicate that growth has continued at a solid pace in Q2, while the OECD expects the economy to expand by 1.8% both this year and next. The improvement in the labour market is continuing apace: employment rose for a 15th quarter in a row in Q1 and the unemployment rate has fallen to 9.3% (April), almost 3 percentage points below its 2013 peak. Headline inflation has been volatile recently and stood at 1.3% in June, while the core rate is hovering just above 1.0%. The ECB left policy on hold in June but, reflecting the better economic situation, dropped its ‘easing bias’ in relation to interest rates albeit it expects them to remain at their present level for an extended period of time. More generally, it reiterated that continued monetary stimulus is needed to ensure inflation returns to target on a sustained basis, though Mario Draghi says the ECB must also be prepared to adjust the degree of stimulus as the economic recovery proceeds. |

|

|

|

UK inflation rises further |

|

The pace of growth in the UK economy slowed to 0.2% q-o-q in Q1 (from 0.7% in Q4 2016), mainly due to more moderate consumer spending. High frequency data suggest GDP growth may be firmer in Q2 but still softer than at the end of last year - retail sales in April-May, for example, were running ahead of their level in Q1, as was the composite PMI. The OECD expects growth of 1.6% this year (after 1.8% in 2016), slowing to 1% in 2018. The unemployment rate has continued to edge lower (to 4.6%), though the year-on-year growth in earnings has slowed and, excluding bonuses, was running at just 1.7% in the three months to April. Annual inflation picked up further in May, rising to a near 4 year high of 2.9%, well ahead of the growth in earnings. The BOE's MPC voted 5-3 to keep interest rates unchanged in June - the dissenters favouring an immediate 25bps hike - and said its tolerance for above target inflation has lessened. Meanwhile, the Brexit negotiations are underway, with disagreement at the outset on the issue of the rights of EU citizens living in the UK. |

|

|

Having slowed in the opening quarter of the year, growth in the US appears to have picked up in Q2. In particular, consumer spending looks to have strengthened having been very subdued in Q1. The OECD expects annual GDP growth to pick up to 2.1% in 2017, strengthening to 2.4% in 2018, though for both years this is lower than previously projected reflecting a delayed ‘fiscal stimulus’. Employment increased by 138,000 in May and the unemployment rate fell to 4.3%, its lowest level in 16 years. Inflation has softened recently with the headline and core PCE rates both falling to 1.4% in May. The Fed believes this may partly reflect 'idiosyncratic' factors and expects inflation to pick up to its 2% target in 2018. It raised interest rates by 25bps in June (to a range of 1.0% to 1.25%) and signalled one further increase is likely this year (to be followed by 3 hikes in 2018). The Fed also set out a plan to gradually reduce the size of its balance sheet, which Janet Yellen said may get underway ‘relatively soon’. |

|

|

|

|

Forward rates are sourced from Bloomberg and are calculated from live prevailing market interest rates and reflect market prcing as at 29/06/2017 |

Disclaimer This document has been prepared by the Economic Research Unit at The Governor and Company of the Bank of Ireland (“BOI”) for information purposes only and BOI is not soliciting any action based upon it. BOI believes the information contained herein to be accurate but does not warrant its accuracy nor accepts or assumes any responsibility or liability for such information other than any responsibility it may owe to any party under the European Communities (Markets in Financial Instruments) Regulations 2007 as may be amended from time to time, and under the Financial Conduct Authority rules (where the client is resident in the UK), for any loss or damage caused by any act or omission taken as a result of the information contained in this document. Any decision made by a party after reading this document shall be on the basis of its own research and not be influenced or based on any view or opinion expressed by BOI either in this document or otherwise. This document does not address all risks and cannot be relied on for any investment contract or decision. A party should obtain independent professional advice before making any investment decision. Expressions of opinion contained in this document reflect current opinion as at 30th June 2017 and is based on information available to BOI before that date. This document is the property of BOI and its contents may not be reproduced, either in whole or in part, without the express written consent of a suitably authorised member of BOI. |

The Governor and Company of the Bank of Ireland is regulated by the Central Bank of Ireland. In the UK, The Governor and Company of the Bank of Ireland is authorised by the Central Bank of Ireland and the Prudential Regulation Authority and subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our authorisation and regulation by the Prudential Regulation Authority and regulation by the Financial Conduct Authority are available from us on request. The Governor and Company of the Bank of Ireland is incorporated in Ireland with limited liability. Registered Office - 40 Mespil Road, Dublin 4, Ireland. |

|

|

|

|